Money the fresh Fantasy: An alternative Agents Help guide to Mortgage loans

- Home School

- Home Licenses

- A residential property Careers

- Real estate market

- Home Money

For people who failed loans Cullman AL to know already which of personal experience, you surely picked up on it easily on your the brand new community: Most homebuyers loans their property commands.

Modern times have seen reasonable rise in the part of bucks even offers since the housing marketplace possess heated up – having NAR reporting a single-seasons increase from sixteen% to help you a peak of 25% inside the . You to nonetheless makes around three-residence off consumers depending on mortgages making its desires away from homeownership a real possibility.

And this as being the instance, you prefer a foundational comprehension of the field of mortgage lending, that’s just what this informative article hopes to incorporate you.

Mortgages 101

The reason for home financing is to let the family customer the immediate great things about homeownership while they spend to about three ages paying the acquisition. And you will mortgage brokers are ready couples within this campaign provided that since their monetary rewards fulfill the risks intrinsic for the extending the new loan.

How they perform all of that will become visible once we look at the elements of a mortgage loan in addition to diversity regarding mortgage loan factors being offered.

Parts of an interest rate

Advance payment: This refers to the cash establish at the start of financing. The traditional advance payment loan providers like to see is 20%e in the having a top down-payment, and debtor may take pleasure in a reduced rate of interest. The alternative is also correct. The reason being an advance payment reduces the lender’s exposure by the making certain the house, hence serves as equity, are more than the borrowed funds number.

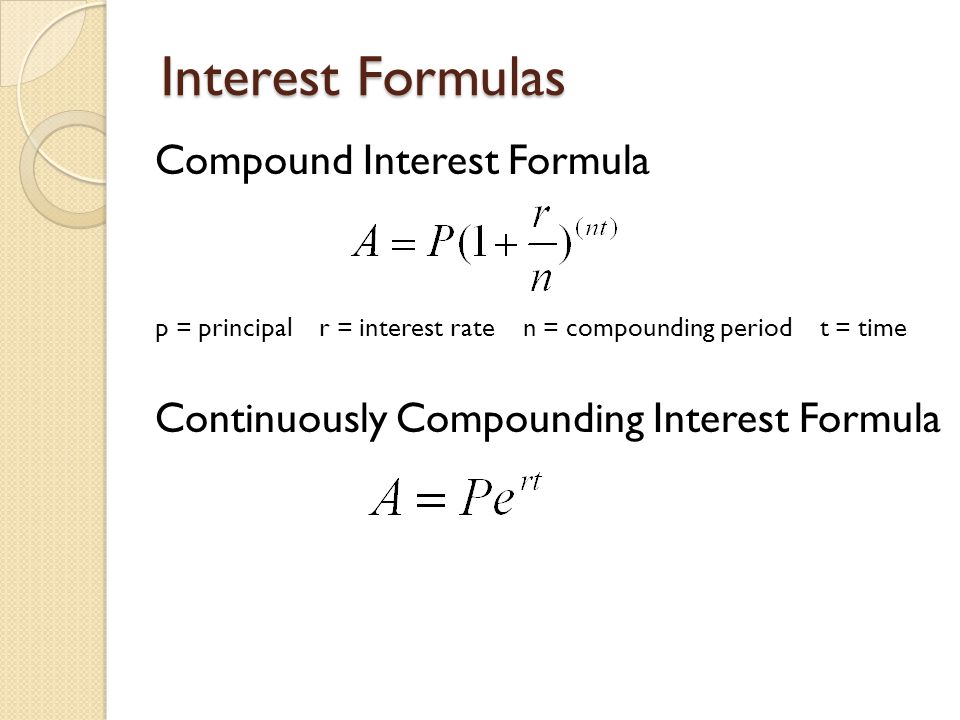

Amount borrowed: Price – Advance payment = Amount borrowed. Told you one other way, the loan matter ‘s the rest of the purchase price. This is the equilibrium in fact it is spread out along side existence of your mortgage, paid-in monthly premiums. Having a vintage totally amortized mortgage, the very last payment pays off of the loan completely.

Interest rate: That is where all of the lender’s award exists. The interest rate ‘s the prices your debtor will pay for the brand new right of the loan. Once more, the higher the fresh perceived risk, the greater the interest rate.

Financing Software

In the event that a lender chooses to stretch financing so you can a debtor, they will certainly seek to match one borrower on the suitable financing system. Here is an easy range of typically the most popular loan programs:

Antique Fund: A traditional financing is not backed by a national agencies. As they require mortgage insurance coverage when your advance payment is shorter than 20%, their attention pricing are aggressive.

FHA Money: Government Housing Government financing are simpler to qualify for, especially for consumers which have lower fico scores, often useful earliest-date homebuyers.

Virtual assistant Funds: A pros Points loan is protected of the You Company out-of Veterans Issues and provides experts several benefits, including all the way down interest levels, no required advance payment, with no financial insurance fees.

USDA Money: United states Institution off Farming financing need no down-payment, which makes them perfect for those people in the place of savings who otherwise meet the program’s advice.

Qualifying to have a mortgage

While a lender is the one to provide them with specified answers, you might enable them to know very well what goes in answering the individuals concerns.

Financial Considerations

When a loan provider evaluates a borrower for financing qualifications, it assemble all the information wanted to create a sound financial choice. They’ll earliest see whether or not the new debtor is actually a beneficial risk they would like to deal with around any circumstances. While so, it determine what financing services terms and conditions he could be prepared to bring.

By looking at this type of activities to each other, a lender may a sense of how well a borrower has fulfilled the loan obligations in past times, how good will they be set-up to take on the additional loan duty a house get provides, and exactly how high-risk tend to the borrowed funds feel toward bank relative into the worth of the house protecting the borrowed funds.

Minimum Qualifications

As far as really lenders are involved, the best borrower was somebody who does not require the mortgage. However the finest debtor isn’t really taking walks in that doorway anytime soon, and more than lenders understand that. Thus, while they may want a great 20% deposit, capable manage consumers exactly who arrive at the brand new table which have lower than one to or whose credit score and you may obligations-to-earnings proportion you are going to log off a small becoming desired.

However, there is a threshold to their mercy and you can facts. Here are a few of the restrictions (minimums otherwise maximums) for the most preferred loan applications lenders work on:

Fortunately that underwriting from mortgages is a mix of art and you may research. The brand new certification and you can limitations revealed over would be fudged some time when it comes to the whole monetary image of the mortgage. But they depict brand new boundaries which have been set since creating affairs.

Other factors Impacting Mortgage Can cost you

Interest rates and you can loans charges was examples of items unrelated so you’re able to this new borrower’s financial reputation that will affect mortgage can cost you. And these can vary notably from bank to help you lender.

Long-label Interest rates

Long-name rates of interest is influenced by trader demand for 10- and 30-year You.S. Treasury cards and you may ties. More this new need for such cards and securities, the low the eye pricing for long-identity fixed-price fund – such mortgage loans.

Since borrower’s credit rating and you may financial status can somewhat dictate the pace they’re going to spend on the mortgage loan, the present price is generated just before in addition they head into this new lender’s office.

And you will, once numerous years of coming to historic lows, mortgages interest levels are starting to tick up once again. So, any type of your own visitors-website subscribers will perform adjust their credit character, the greater away from they are.

Apr (APR)

Annual percentage rate ‘s the annual cost of a loan in order to a debtor, including costs, shown given that a percentage. As opposed to mortgage, not, Annual percentage rate comes with most other charges otherwise fees linked to the mortgage, such as home loan insurance rates, of many closing costs, write off circumstances, and origination costs.

The brand new moral of your own tale the following is the genuine costs out of financing from one bank to the next may vary notably even when the interest being offered is similar. Therefore, definitely teach your clients as to how evaluate mortgage even offers that seem is similar. Hear you to definitely Annual percentage rate!

So what can You will do?

To have client-website subscribers looking for capital, your position is to instruct and you may ready yourself them for just what are to come. Here are some steps you can take:

Has actually a frank dialogue regarding your consumer’s economic character, telling all of them of the economic recommendations and is affirmed by one financial considering all of them for a financial loan.

Go the consumer from math of financial obligation-to-money proportion observe what type of monthly mortgage repayment it you’ll carry out.

Останні коментарі